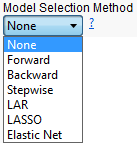

Use this drop-down menu to select the method to be used for selecting the final

predictor

variables.

|

Choose this option to use all of the

variables

and backward starts with all of them

Caution

: Choosing this option can result in long run times when there are thousands of variables.

|

|

|

Choose this option to perform a forward search, beginning with no variables in the

model

and adding the most significant ones one at a time.

|

|

|

Caution

: Choosing this option can result in long run times when there are thousands of variables.

|

|

|

Choose this option to perform a least-angle regression

1

, which begins with no effects. The parameter estimates at any step are shrunken when compared to the corresponding least squares estimates. If the model contains classification variables, then these classification variables are split.

2

See the SPLIT option in the CLASS statement of SAS PROC GLMSELECT for details.

|

|

|

Choose this option to add and delete parameters based on a version of ordinary least squares where the sum of the absolute

regression

coefficients is constrained

3

. If the model contains classification variables, then these classification variables are split.

2

|

|

|

Choose this option to augment the data and use a LASSO fit in accordance with an Elastic Net.

4

|