This example uses the SeriesP.jmp sample data table to show how to perform a time series analysis. You first create a new column that is appropriate for the Time ID.

|

1.

|

The SeriesP.jmp data table contains a Year column and a Quarter column to identify the time period during which the responses were observed. However, the Time Series platform requires one column with unique, equally spaced time points to label the X axis. If no Time ID is specified, then the row number is used to identify the time periods. To avoid this and make the report easier to interpret, you construct a Time ID column from Year and Quarter.

|

2.

|

|

3.

|

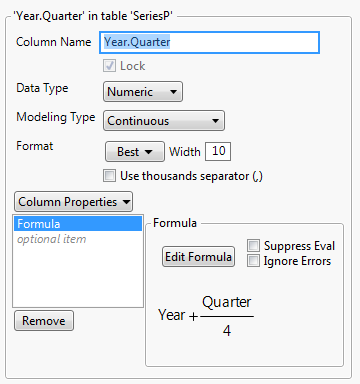

Select Column Properties > Formula.

|

|

4.

|

Select Year and then click the plus sign.

|

|

5.

|

|

6.

|

Click OK.

|

Figure 15.16 New Column

|

7.

|

Click OK.

|

|

1.

|

Select Analyze > Specialized Modeling > Time Series.

|

|

2.

|

|

3.

|

|

4.

|

Click OK.

|

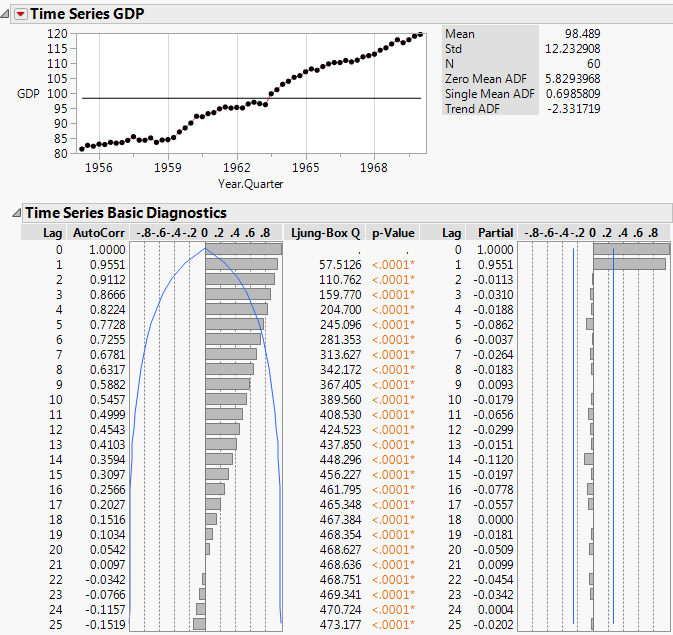

Figure 15.17 Time Series Report for SeriesP.jmp

|

5.

|

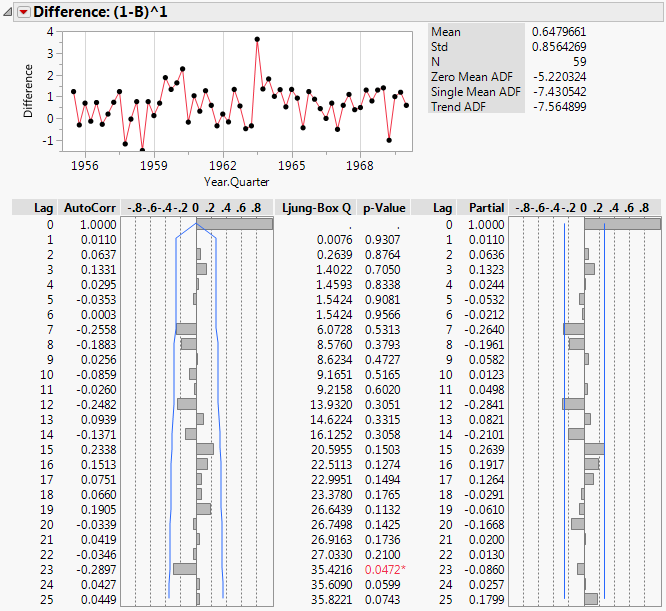

Figure 15.18 Difference Report for SeriesP.jmp

|

7.

|

Click the Time Series GDP red triangle and select Smoothing Model > Linear Exponential Smoothing.

|

|

8.

|

Click Estimate.

|

|

9.

|

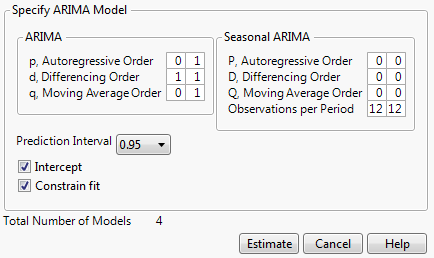

Click the Time Series GDP red triangle and select ARIMA Model Group. This enables you to fit multiple ARIMA models for a range of values of (p,d,q)(P,D,Q).

|

|

–

|

Fix d, the differencing order, at 1 by setting the range from 1 to 1 because the differencing report showed lag-1 differencing was appropriate.

|

|

–

|

Set p, the autoregressive order, to range from 0 to 1 because the original series showed evidence of autocorrelation.

|

|

–

|

Set q, the moving average order, to range from 0 to 1.

|

|

–

|

Figure 15.19 ARIMA Model Group Specification

|

11.

|

Click Estimate.

|

Figure 15.20 Model Comparison Table

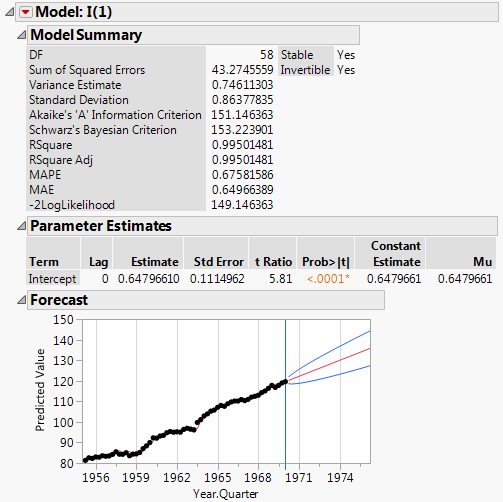

Figure 15.21 Model Report for ARIMA(0,1,0)