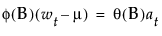

t is the time index

μ is the intercept or mean term

φ(B) and θ(B) are the autoregressive operator and the moving average operator, respectively, and are written as follows:

at are the sequence of random shocks

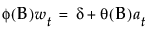

The constant estimate δ is given by the relation:

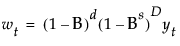

In the case of Seasonal ARIMA modeling, the differencing, autoregressive, and moving average operators are the product of seasonal and nonseasonal polynomials:

where s is the number of observations per period. The first index on the coefficients is the factor number (1 indicates nonseasonal, 2 indicates seasonal) and the second is the lag of the term.