Modeling Specifications

The Modeling Specifications report enables you to fit models to the individual time series. A variety of models are considered. Hyndman et al. (2008) defines state space smoothing models based on their error, trend component, and seasonal component:

• The errors can be additive (A) or multiplicative (M).

• The trend component can be none (N), additive (A), additive damped (Ad), multiplicative (M), or multiplicative damped (Md).

• The seasonal component can be none (N), additive (A), or multiplicative (M).

A specific model can be represented by its ETS (Error, Trend, Seasonal). These are the models used in Time Series Forecasting.

There are two tabs in the Modeling Specifications report. Use the Recommended Specifications tab to fit a set of state space smoothing models that is chosen by the platform. Use the Complete Specifications tab to select the specific state space smoothing models that you want to fit. For each individual time series, the best fitting model from the given set is then used for forecasting.

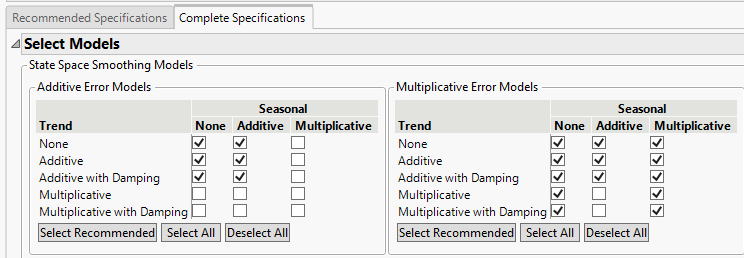

Select Models

Available only in the Complete Specifications tab, shown in Complete Specifications Tab. The Select Models report enables you to specify the state space smoothing models to fit to the individual time series. Use the check boxes to select the error, trend, and seasonality for the models. Click Select Recommended to select the check boxes that correspond to the models recommended by the platform. Click Select All to select all check boxes or Deselect All to deselect all check boxes.

Figure 18.5 Complete Specifications Tab

Forecast Settings

Enables you to specify the following optional settings:

NAhead

Specifies the number of steps ahead to forecast. The number of steps must be nonnegative.

Period

Specifies seasonality values to be considered in the model fitting process. By default, the period is set to the suggested seasonality from the Analysis of Time Pattern report. If you want to consider models with different seasonality, specify the additional periods here and separate them with a comma. The period must be greater than zero.

NHoldout

Specifies the duration of the holdout series used for validation. This value must be nonnegative.

Other Options

Enables you to specify the following options:

Preserve Model Selection Criterion

Saves the model selection criterion for the set of models that is fit to the data. After model fitting, this information is shown in the Information Criterion of All Models for All Series report.

Forecast Interval Level

The prediction interval level for the forecasts. This changes the width of the shaded area in the forecasting plots.

Imputation for Applicable Models

Specifies the imputation method used during the model fitting process.

Note: These options change only the data that are used for model fitting. The raw data are not changed.

None

Does not impute missing values.

Last Value

Imputes missing values by using the last value that is available before a sequence of missing observations.

Middle Value

Imputes missing values by averaging the last value that is available before a sequence of missing observations and the first value that is available after a sequence of missing observations.

Linear Interpolation

Imputes missing values by creating a linear interpolation between the last value that is available before a sequence of missing observations and the first value that is available after a sequence of missing observations.

When you click Run, the specified set of models is fit. When the fitting process is complete, the Model Reports report is shown. See Model Reports. If you make any changes to the options in the Model Specifications report and click Run again, the Model Reports report is replaced with a new report.